Value Chain Analysis

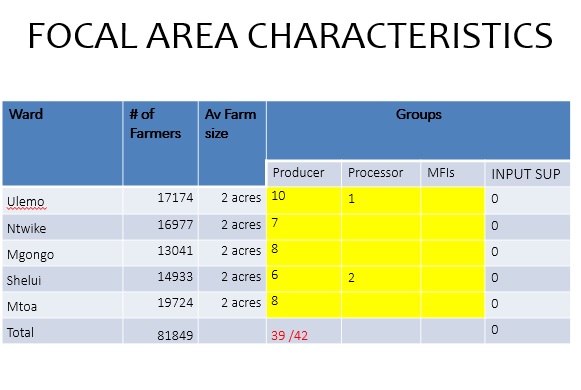

The main objective of the analysis was to understand the functioning of the sunflower subsector, identify potential opportunities to develop the sub-sector into viable value chains beneficial to small holder farmers in Iramba district. This was based on baseline assessment and demand trends, potential to increase household income, private sector engagement, potential to enhance inclusiveness in terms of gender and youth. The analysis involved all the sunflower chain actors mainly producers from the PEML program area in Iramba District covering five wards, namely Ulema , Shelui ,Mtoa , Mgongo and Ntwike, as well as processors, brokers and retailers from Iramba and neighboring areas. Actors from neighboring areas other than Iramba were also interviewed because their actions have a direct linkage and effect to the sunflower producers in Iramba district.

Over the last three months, RCCL team has undertaken a number of activities related to the project focusing on areas with potential to grow sunflower in the five pre-selected wards. In addition to the main chain actors an identification of appropriate services to support the development of the sunflower sub-sector was undertaken by collecting useful information from chain supporter. The data was collected to obtain a strong basis for understanding key industry trends and issues specific to the sunflower market system. Also mapping exercise to depict how products flow through the sub-sector systems as well as the interrelationships between different actors.

Over the last three months, RCCL team has undertaken a number of activities related to the project focusing on areas with potential to grow sunflower in the five pre-selected wards. In addition to the main chain actors an identification of appropriate services to support the development of the sunflower sub-sector was undertaken by collecting useful information from chain supporter. The data was collected to obtain a strong basis for understanding key industry trends and issues specific to the sunflower market system. Also mapping exercise to depict how products flow through the sub-sector systems as well as the interrelationships between different actors.

Study Findings

Seed Variety

From the analysis it was obvious that there is a great disparity between the farmers understanding of the market requirements and the actual market requirements. While processors log for sunflower variety with high oil content farmers on the other side are busy producing varieties that can fill the bags more easily. This misunderstanding has prolonged the poor productivity f sunflower; farmers keep on relying on recycled seeds while buyers are keen on the seed varieties which the most preferred one is Kenya Fedha which is said to have high content of oil and thus suitable for processing. From the diagram below channel one of intergraded small scale producers those using improved seed variety actually referred to the Kenya Fedha and record variety while the rest is quality declared seeds and recycled seeds. While for the second channel seed variety refereed is Kenya Fedha and record alone. There is a general shortage of quality sunflower seeds country wide. According to (RLDC 2008) in the central corridor it is estimated that only 35% of sunflower farmers use certified Quality Seeds or Quality Declared seeds (QDS) while in Iramba less than 5% for the farmers actually use improved seed (baseline survey 2015).It is therefore important to increase the production, distribution and awareness of quality seeds so that more farmers can move away from recycled to improved seeds, and therefore increase their productivity level. From experience quality seeds have the potential to increase productivity from five bags to 20 – 25 bags per acre.

Actors in Value Chains

Sunflower Value Chain Map

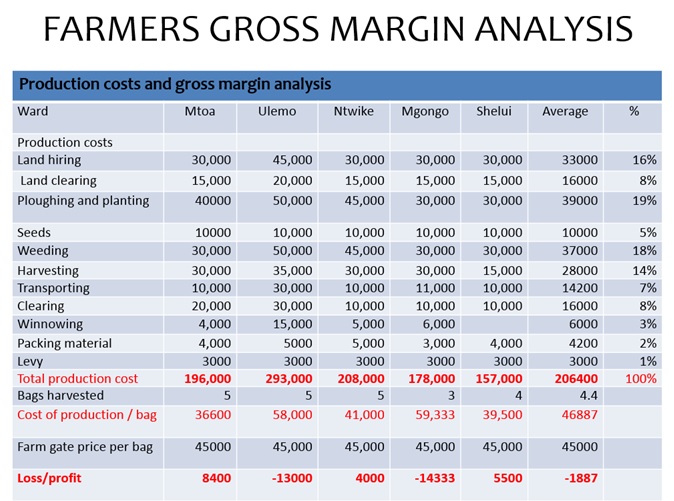

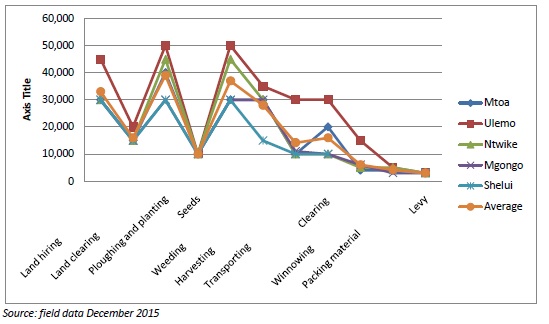

Sunflower Production Costs between Five Wards

Sunflower production in Iramba varies from one are to the other, even the different cost items vary from one ward to the other. The diagram below indicates the costs of production between the five selected wards of Ntwike, Shelui, Mtoa, Ulemo and Mgongo. While Ulemo and Ntwike indicated a relative high cost of production compared to Shelui and Mgongo which has the lowest cost of production, Mtoa is close to the average cost of production between the wards. It costs more in Ulemo to hire a one acre land than the cost of the same land in Mtoa and elsewhere. Another cost category with the highest cost is the cost of ploughouing and planting it costs more in Ulemo and Ntwike TZS 50,000 and 45,000 while it costs 40,000 in Mtoa and only 30,000/= in Mgongo and Shelui. On average the highest cost items in production are land, ploughouing and planting and weeding. While the lowest cost are related to village levy, parking materials and winnowing. It should be noted that most of these cost items are not recorded by individual farmers or household, and most of the cost items are covered by family labor although in some cases hire laborers are engaged to do the work. In some cases the extension officers keep records for the Farmer Field Schools plots operated in the area.

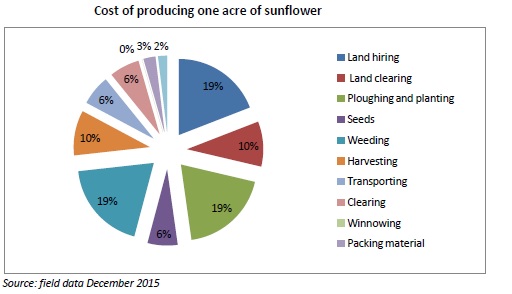

Cost of producing one acre of sunflower

The diagram below presents the different cost items in producing once acre of sunflower, land, planting and weeding take most of the costs. This diagram compares the costs, revenues and gross margins between the selected wards. The cost of production is relatively higher than the revenue generated in Ulemo and Mgongo thus causing a negative gross margin, while the overall gross margins in all the wards is relatively low compared to the costs and revenue generated.

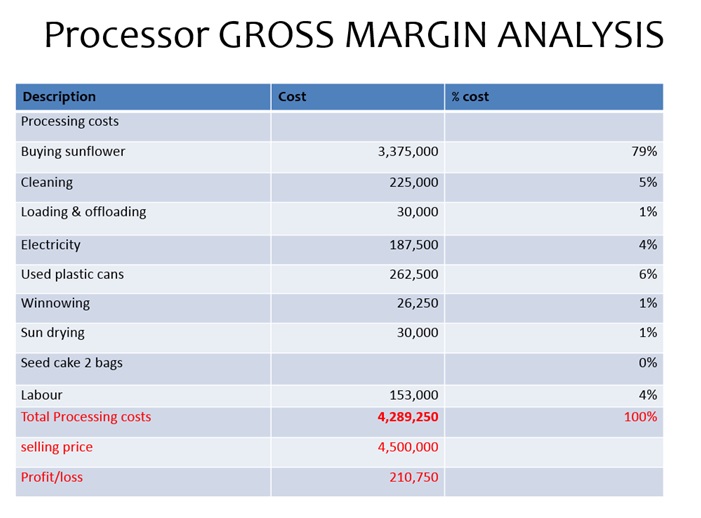

Processing Costs

Processors employ a broker at the farm to collect and do all the buying arrangements for them. From the analysis conducted the diagram below presents the different costs associated with the Al Kazroon Company ltd a processor located in Shelui ward, from the diagram and field data the processor incurs 79% of the total cost associated with processing on buying sunflower seeds. Other costs associated with processing include clearing sunflower before the actual processing 5%, Loading and offloading 1%, Electricity 4%, causal labors for drying and winnowing 5% in total, as well as plastic containers for the oil 6%. Below is a pie chart indicating all the costs, with the purchase of sunflower taking the biggest margin of all the costs associated with processing.

The diagram below indicates the costs, revenues and gross margins between the actors, the farmer (producers0 and the processors in this case. The example is taken from Shelui ward simple because of all the processors Mr. Adbul Mohamed who owns a procession facility under the business name of the Al Kazroon Company Ltd was more cooperative in the analysis compared to other processors who thought the whole exercise I just a waste of time for them with the exception of Mr. Elifadhili Ezekiel of Ulemo ward who also owns a processing facility under the name of Shangai sunflower Oil Mills Ltd.

From the diagram producers incurs 19% as total production costs, while processors incurs 27% as total processing cost. Of these producers make revenue of 21% thus leaving 3% as profit generated. While processors make revenue of 29% thus making a profit of 2%. Generally the margins associated with production and processing seem to be very low compared to the average margin one can make in business. On the farmer this situation is highly attributed by the lack of use of improved seeds, proper agronomic practices and selling immediately after harvest when prices are at the lowest. While the inefficiency on the processing is mainly caused by poor post a harvest techniques by farmers, processors need to start cleaning and winnowing the produce again before the crashing takes place all these impose a cost in doing business. Processors cannot charge a higher price in the market to carter for the production cost because there is s high chance and big risk to lose the market to imported crude oils, or unregulated small scale processing activities.

From the diagram producers incurs 19% as total production costs, while processors incurs 27% as total processing cost. Of these producers make revenue of 21% thus leaving 3% as profit generated. While processors make revenue of 29% thus making a profit of 2%. Generally the margins associated with production and processing seem to be very low compared to the average margin one can make in business. On the farmer this situation is highly attributed by the lack of use of improved seeds, proper agronomic practices and selling immediately after harvest when prices are at the lowest. While the inefficiency on the processing is mainly caused by poor post a harvest techniques by farmers, processors need to start cleaning and winnowing the produce again before the crashing takes place all these impose a cost in doing business. Processors cannot charge a higher price in the market to carter for the production cost because there is s high chance and big risk to lose the market to imported crude oils, or unregulated small scale processing activities.